May 2026

Investment Strategy

4 min read

Market Overview

Middle East developments again dominated investor attention in May. Mounting optimism over a potential US–Iran agreement eased fears of a prolonged conflict — and, with them, the stagflation concerns that had weighed on sentiment. Brent crude fell 19.3% over the month, its steepest monthly decline since March 2020, as the prospect of de-escalation unwound much of the war-risk premium that had accumulated since February.

Risk assets rallied in response. The S&P 500 rose 5.3% to a record high, with semiconductors leading on renewed AI enthusiasm: the Philadelphia Semiconductor Index (SOX) gained 22.2% in May, extending its year-to-date advance to 81.5%. The move was more pronounced still in South Korea, where the KOSPI surged 28.5% on the month, lifting its year-to-date gain to 102.4%. (1)

Sentiment turned more cautious in mid-May, as sovereign bond yields climbed to multi-year highs amid renewed concerns over persistent inflation and uncertainty surrounding the new Fed Chair’s policy stance. With real yields rising and inflation-hedging demand fading, gold fell 1.5% — its third consecutive monthly decline.

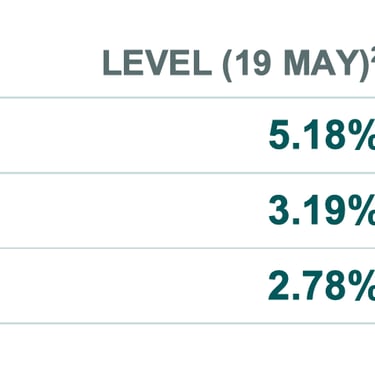

The Yield Spike

Since the onset of the US–Iran conflict in February, higher fuel prices have pushed up inflation expectations and government bond yields. The move accelerated sharply in mid-May, with several benchmark yields reaching their highest levels in years:

The composition of the move, however, points to a more nuanced driver. Between end-April and midMay, the roughly 30bp rise in nominal yields was matched by a roughly 27bp rise in real yields leaving breakeven inflation, and therefore long-term inflation expectations, essentially unchanged. This suggests the sell-off was driven less by oil-linked inflation than by concerns over the scale of the US fiscal deficit and uncertainty over the policy direction of Fed Chair Warsh.

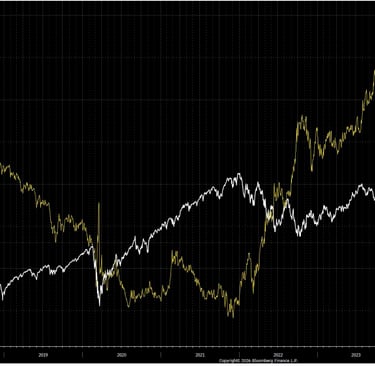

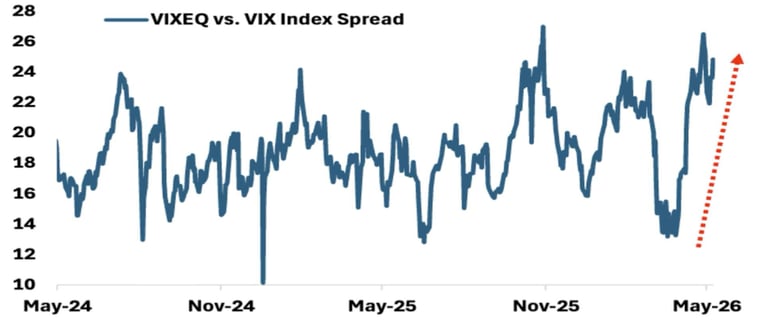

Two technical signals warrant close attention: the pace of the yield increase (Chart 1) and unusually wide dispersion at the index level (Chart 2). A recent CBOE report highlights elevated single-stock dispersion beneath a relatively calm index surface; historically, an extreme gap between the VIX and its equal-weight counterpart (VIXEQ) has tended to precede short-term equity corrections.

Chart 1: Real yield vs. S&P 500 (3)

Chart 2: Divergence between stock vs. index vol (4)

Positioning

Against this backdrop, we maintain a defensive tilt while staying alert to tactical opportunities:

– Cautious on US mega-cap equities and long-duration credit, where stretched valuations and rate sensitivity leave little margin for error.

– Favour international equities, short-dated Treasury notes, and longer-tenor commodity contracts.

– Opportunistic on gold, looking to add on further weakness.

SOURCE:

1Data is obtained from Bloomberg, as of 29/5/20262

2Data is obtained from Bloomberg, as of 19/5/2026

3 Source: Bloomberg

4 Source: CBOE

Advertisement Disclaimer

The information presented here is intended for Accredited or Institutional Investors only and it does not constitute a recommendation to anyone; it also has not taken into account the specific investment objectives, financial situation or particular needs of any particular person. Information herein is based on sources we believe to be accurate and reliable as at the date it was made. We reserve the right to revise any information herein at any time without notice. No offer or solicitation to buy or sell securities, funds or products and no investment advice or recommendation is made herein. In making investment decisions, investors should not rely solely on this advertisement but should seek independent professional advice. However, if you choose not to seek professional advice, you should consider the suitability of the investment for yourself. Past performance of the fund manager, portfolios, and the funds are not indicative of future performance.

Investment involves risks including the possible loss of principal amount invested and risks associated with investment in emerging and less developed markets. The fund manager, portfolios, and the funds may invest in illiquid instruments, financial derivative instruments and/or structured products and be subject to various risks (including counterparty, liquidity, credit and market risks etc.). Investing in fixed income instruments (if applicable) may expose investors to various risks, including but not limited to creditworthiness, interest rate, liquidity and restricted flexibility risks. Changes to the economic environment and market conditions may affect these risks, resulting in an adverse effect to the value of the investment. During periods of rising nominal interest rates, the values of fixed income instruments (including short positions with respect to fixed income instruments) are generally expected to decline. Conversely, during periods of declining interest rates, the values are generally expected to rise. Liquidity risk may possibly delay or prevent account withdrawals or redemptions. Environmental, Social and Governance (ESG) strategies consider factors beyond traditional financial information to select securities or eliminate exposure which could result in relative investment performance deviating from other strategies or broad market benchmarks. Past performance, or any prediction, projection or forecast, is not indicative of future performance. The duplication, publication, extraction, or transmission of the contents, irrespective of the form is not permitted, except for the case of explicit permission by Aevitas Capital Management Pte. Ltd. This advertisement has not been reviewed by the Monetary Authority of Singapore (MAS).

Contact Us

contact@aevitas.sg

61 Robinson Road #20-01, 61 Robinson Singapore 068893